In 2009 I bought a 5-year bond issued by IFFIm – the International Finance Facility for Immunisation. I invested £5000 and received £5810 a few days ago (with accumulated interest). Not the best return on capital in history, but not bad considering current interest rates and the intervening financial crisis. The bond was AA-rated with sovereign guarantees from the UK, France, Italy, Norway, Australia, Spain, Holland, Sweden and South Africa. Pretty safe basically. The other perk was that for every £1000 invested they guaranteed to vaccinate 130 kids. So, my £5k resulted in £810 in interest and 650 kids vaccinated. Not bad for filling out a form.

I work in microfinance. I am aware of the (mostly mediocre) results we are discovering as a sector regarding our own impact upon poverty. I am also aware of the crises that periodically land the sector in trouble, and the dangers of over-indebtedness amongst clients. It irritates me to see the poor having to cough up interest rates of 150% in the name of poverty alleviation. I was appalled at the cases of abuse in Andhra Pradesh. I was not surprised when the Nicaraguan microfinance sector collapsed, and am watching with morbid curiosity as the sectors of Peru and Mexico reach dizzying heights of over-indebtedness and recklessness.

The key question is whether £5000 invested in microfinance would have had a greater or lesser impact than the same sum lent to the GAVI Alliance and used to vaccinate children. We can debate about the subtleties of impact measurement techniques all day, but what concerns me is that the question is not even asked. Is the impact of 650 vaccinations for kids greater or less than the impact of £5000 lent to their parents?

According to the latest World Bank paper on the topic, consumption increases by 0.42% in Bangladesh as a result of microloans. So, £5000 in loans would increase consumption by roughly £20. Is that better than vaccinating 650 kids? Obviously these two outcomes cannot be directly compared, and ideally we could do both. Investors in for-profit microfinance institutions might find lending more attractive than vaccinations, as they can earn substantially higher returns. But what do the poor think?

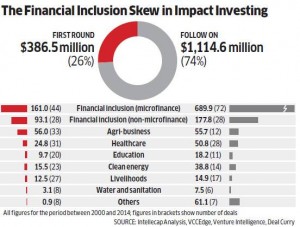

The microfinance sector is approaching the $100 billion mark. That is a chunk of money and it is reasonable to ask whether microfinance has been the best deployment of this capital. The argument over whether microfinance works or not is a red-herring. The key question is whether this is the wisest use of scarce capital. In all other areas of economics, projects or interventions are compared to their next best alternatives. But not in microfinance.

No one is asking these awkward questions, least of all the people who run the microfinance sector. As David Roodman pointed out, we have created a “microfinance industry”. Industries have vested interests and lobbyists. Do we really expect Grameen, Accion, Opportunity, Smart, Finca, Kiva etc. and the microfinance fund managers to ask these questions? Their opinions are foregone conclusions when their very existence (and salaries) depend on the endless expansion of microfinance.

The only article I have seen directly tackling this question was by Paul Polak and Mal Warwick, authors of The Business Solution to Poverty. They make an astute observation analysing where social impact investors are directing their capital:

“In our view, microcredit is one of the least worthy fields in social enterprise. That so much of the scarce resources available to address the challenges of poverty and climate change is squandered on for-profit microfinance ventures is a tragedy. While some microcredit programs — principally those operated as nonprofits — have achieved a lot of good, the rush by the big banks and profit-minded entrepreneurs into the field has proven to be a curse, not a blessing.”

Perhaps the two great tragedies of microfinance are as follows:

1) We have deployed vast sums of capital with modest outcome. This may have been more effective in other areas.

2) The sector refuses to address these simple questions in a quest to protect itself from the rigours of scrutiny.

Some microfinance is good, effective and ethical. But has the sector grown too large, and risks crowding out more effective interventions? This is surely a valid question?

{kind=link}