[This is a detailed review of an academic paper. For a summary of this blog-post, click here].

A recent paper has attracted attention, likely to garner support from microcredit supporters. Firstly, it was written by prestigious academics from well-known institutions (Yale, Dartmouth, Innovations for Poverty, thanking many of the industry heavyweights in the process – Banerjee, Duflo, Adams, Roodman etc). Secondly, it focuses on a polarizing institution – Mexico’s Banco Compartamos. The bank caused uproar in 2007 for an extremely profitable IPO, charging the poor high interest rates (up to 195% by some measures), and for huge payouts to certain individuals. This prompted some to wonder if profit had become detrimentally dominant in the sector. “They’re absolutely on the wrong track,” said Muhammad Yunus. “Their priorities are screwed up.” Thirdly, and perhaps most critically, the results seem superficially positive – microcredit is helping the poor after all, even at Compartamos.

However, upon closer scrutiny, the results are surprisingly pessimistic. The paper is complex and I struggled to understand all the econometrics involved. In some regards this resembles the famous Pitt and Khandker 1998 paper: it appears to support the core premise of microfinance, but as one digs deeper such conclusions are a little more “fragile” than one might suspect. For example, David Roodman discovered that by removing 16 outlying observations (of a total of 5,218) in the P&K sample the positive impact of microfinance vanishes. Hardly reassuring. Further doubts of P&Ks findings were published by Duvendack and Palmer-Jones (2012). Debate ensued perhaps because the paper had been so influential in justifying microfinance.

I will describe the current paper in layman terms and share some thoughts on it. My conclusion is simple – this is a rigorous paper that extracted every positive element possible from the dataset, and should be read with interest and caution in equal measure.

The paper

The authors use a randomized control trial (RCT) methodology. This is widely considered to be a valid experimental technique for such investigations, although it does have critics (amongst them, Angus Deaton of Harvard). In essence, the method splits the sample into those who receive a loan and those who don’t (similar to a “control group” in medical experiments), and looks at the differences between the two. In reality it is a little more complex. The subtleties of possible flaws in the methodology is not my prime concern here – what worries me are the results presented.

The authors worked alongside Compartamos in the northern Mexican state of Sonora state, ranked 9th of 31 states with a GDP per head of $10.336 in 2007. They made loans to some of these clients, exclusively to women, at APRs of roughly 110% APR. The market interest rate is apparently 100% (page 2 – the authors cite no source for this claim). Quite whether this APR includes the cost of VAT and forced savings is unclear. David Roodman analysed the interest rates charged by Compartamos (see his table below) and demonstrated succinctly how an uncompounded annual interest rate of 79.13% increased to 87.03% when forced savings were considered. When the cost of VAT is included the rate increases to 101.1%. Considering the effect of compounding increases the APR to 195%. There is no mention in the paper of either forced savings or VAT, so I have no idea exactly what this stated APR of 110% refers to. The Compartamos website suggests the rate APR is 77.6% excluding VAT, with no mention of forced savings. Finally, clients repay loans at a bank or convenience store (page 6) and there is no mention whether this is at the expense of Compartamos or the client. Bank transfers are relatively expensive in Mexico, and this could increase the total cost of loans yet further.

Their findings are mixed but the overall conclusion is positive. The paper is fairly balanced, and while the impression I get is that the authors extract every ounce of positivity they can from the frankly mediocre findings, they do state that there is simply very little evidence of much impact on a number of key variables. The glass is half full.

“Some good and little harm” (abstract & page 3).

“There is evidence of both increased investment and improved consumption smoothing” (page 3).

“Happiness, trust in others, and female intra-household decision power also increase” (page 3).

“Overall we do not find strong evidence that the credit expansion creates large numbers of ‘losers’ as well as winners” (page 4).

The dangers of over-indebtedness and a lack of positive impact upon poverty are mentioned as the potential pitfalls of microfinance. This is a narrow view of the potential harm that microfinance could conceivably have. Readers of Bateman will be familiar with his criticisms that microfinance trivializes the industrial base of countries and limits the formation of small and medium enterprises. Capital used to finance microfinance portfolios, including mobilized savings, could have been deployed in other developmentally focussed ways with a greater impact on the long-term health of the industrial base of a nation and create meaningful jobs. Such funds are instead deployed creating hordes of trinket-vendors. Such arguments are hotly debated, but make no appearance in this paper.

Microfinance sceptics have suggested that crowding out, or employment displacement, or as the authors of the paper label the phenomenon – “business stealing” (page 1), is a serious risk, and yet the paper barely discusses the phenomenon. They claim on page 3 that their analysis measures the total impact on the community, and not just of their subjects, and yet I was not convinced this was the case. Entire neighbourhoods are flooded with loans, and yet not a single incumbent entrepreneur was driven out of business by this influx of capital? There is no mention of such adverse effects. Instead they simply state that “Our estimated effects on the treatment group, relative to control, are net of any within-treatment group spillovers from borrowers to non-borrowers”. Er, please explain. This seems like quite a major claim (or assumption).

Then we come across an interesting reference which touches on one of the central myths of microfinance: loans to the working poor. Microfinance finances entrepreneurs, we are generally led to believe. Compartamos’s own mission statement defines microfinance as “financial services that offer productive people at the base of the pyramid, access to loans, savings accounts, insurance and other services that help develop their businesses and families”. The emphasis is upon creating or building businesses. This is the mantra of microfinance. And yet the paper clearly states that Compartamos “targets working-age women who operate a business or are interested in starting one”. They don’t actually need to be either working (merely old enough to do so), or have a business (merely curious to start one).

The authors expand on this point on page 4: “100% of borrowers are women but we estimate that only about 51% are ‘microentrepreneurs’.” Page 5 elucidates further regarding the underlying activities of the clients: “business activities (or plans to start one) are not verified [by Compartamos]”. Whether the client is engaged in any activity at all appears of such little interest to Compartamos that they don’t even verify the existence of such activities. Nor does it appear of much interest to the authors of this paper. To be included in the study the client had to answer yes to any of the following questions: do you have a business, do you want to start a business, or do you just want a loan?

Many people mistakenly believe that microfinance is used predominantly (if not exclusively) to finance businesses – respect to the authors here – they clearly state that much of this capital is not used for entrepreneurial activities at all – a vital message that the mainstream media and general public usually ignore.

However, this lack of interest in the underlying activities of clients is not to suggest that Compartamos doesn’t have a formal mechanism of carrots and sticks to ensure clients repay loans. Group pressure is the principle means (joint liability). But intriguingly the authors explain on page 5 that the credit bureaus are useful: “Compartamos does pull a credit report for each individual and automatically rejects anyone with a history of fraud. Beyond that, loan officers do not use the credit bureau information to reject clients”. However, on page 6 the authors state that “Compartamos also reports individual repayment history for each borrower to the Mexican Official Credit Bureau”. So, the credit history of the client is irrelevant in the loan application process, but if they fail to repay a loan they are reported to the credit bureau and their credit rating, and thus ability to access other services, is threatened. There is nothing inherently wrong with this, but it sheds some light on the priorities of Compartamos and their strategy: we don’t care about your other borrowings, but beware of non-repayment! The credit bureau is useful to them, but as a threat.

Apparently 9.8% of groups in general are delinquent for more than 90-days (page 6) and are therefore reported not only to the credit bureau but are sent to a collection agency, but the overall default rate is only 1%. Let’s not overlook this fact – 1 in 10 groups struggle to successfully repay a loan. Delinquent members suffer a credit bureau downgrade of some sort – is this a sign of the great success of microfinance? Maybe Compartamos manages to eventually recover 99% of all loans, that’s great for the bank and its shareholders, but 1 in 10 groups have missed a payment by over 90 days – something is clearly not going that well for a significant number of people.

And strangely in this paper, there is very little discussion of default or PAR. Indeed, if measuring the impact of a loan upon clients, including such esoteric measures as “life and harmony index”, surely two potentially negative and easily measured impacts are “client didn’t repay loan” and “client reported to credit bureau”. These were not measured for some reason. We hear plenty about female empowerment in decision making, but if a woman is no longer able to get a phone contract because she’s blacklisted at the credit bureau for missing a repayment to Compartamos, this is a worrying secondary effect ignored in this paper.

Then, on page 2, a stunning statistic emerges. Only 18.9% of those offered loans actually take one. Put it another way – 81.1% are not interested in taking out a loan. In the panel sample it is even lower, at a mere 11.9% (page 10, i.e. 88.1% not interested). And yet we are told on the same page that “returns to capital in Mexico are about 200% for microentrepreneurs”. Hang on, there’s something wrong here. The experiment is conducted in a region where Compartamos was not previously operating, the authors demonstrate that over-borrowing is not a problem in the region (average number of loans per client in entire sample: <1), the poor face 200% returns on capital, and yet over 4 in 5 can’t be bothered to take out a loan even when someone comes knocking on their door offering one – is that normal? This is hardly supporting evidence of the “absurd gap” between the limited supply of credit and the huge pent-up demand.

Research Design, Implementation, and Data

It transpires that only the clients in the outlying areas of Nogales are included in both the baseline and follow-up surveys, so I wonder how representative this is of the entire region. I am relatively unfamiliar with the complexities of RCTs, but I thought the idea was to mix clients up randomly so they are spread out over the entire region, to exclude any effects that may be specific to one region.

They basically did two surveys – a baseline to 2.912 respondents, and an endline to 16.560 respondents. Combining these two led to the panel sample of 1.823. But this means that 1.089 of the baseline respondents were not included in the endline survey. Why not? Did they drop-out between the two surveys (hardly encouraging)? Or maybe they all were surveyed, but for some reason rejected from the actual panel survey. I couldn’t find any explanation of this.

The only other point which jumped out at me in this section was on page 10: “70% of borrowers in the treatment group borrowed more than once”. Given that the project spanned only 2 years or so, and loans are for only 16 weeks, certainly for the 30% who borrowed only once in this period it is hardly surprising that the authors didn’t find much impact. How much impact can a 16-week, $600 loan have on a client, who probably doesn’t even have any sort of micro-enterprise, over a 2 year period?

Identification and Estimation Strategies

This is the technical part of the paper, I’ll skip over this. Only one aspect of this section seemed noteworthy (and I understood!). While discussing the approach for detecting winners and losers (the title of the paper), the authors kindly warn the reader: “recall, however, that [we] have panel data on only about 11% of our sample and for a subset of outcomes” (page 12). Why was 89% of the sample ignored? Because 89% of clients offered a loan didn’t want one. It would be nice to see some additional discussion on this rather awkward point. It appears to have been rather delicately brushed under the carpet.

Results

This is the most interesting section. It roughly follows the order of the data tables provided at the end of the paper:

Tables 1 and 2

These present the base data. Most of the statistics quoted are self-explanatory. “[O]ur survey respondents are observably similar across treatment and control clusters” (page 8) – this is true with regards most variables. However, it was interesting to see that 24.4% of the 16.560 endline sample were prior businesses owners, while 48.8% of the panel sample had prior businesses (see columns 1 and 4 in table 1 for “prior business owner” row). Those in the panel sample were exactly twice as likely to be “entrepreneurs” – quite a major difference in my opinion. Perhaps not surprisingly, those who were previous business owners were approximately 10% more likely to take up a loan than those who were not. Also, it appears that three quarters of respondents had never been a member of a savings group.

Table 3

They find evidence of crowding-in of loans, i.e. those that take loans from Compartamos (average size is $645) tend to increase their total borrowings by $1.248. The authors interpret this in a vaguely positive manner: “these results suggest that there was little substitution of Compartamos loans for other debt”, i.e. it was not the case that clients who borrowed from Compartamos reduced their borrowings elsewhere. This may be a relief to other lenders in the region, but it does raise some questions about over-indebtedness. But other items in Table 1 are interesting:

- There is no significant decline in the amount clients borrow from moneylenders. I thought microfinance replaced the evil moneylender? Shouldn’t we expect those so blessed with loans from Compartamos to borrow less from moneylenders? If the moneylenders charge such incredibly high interest rates as often claimed, presumably flooding the market with comparatively cheap (110% APR) Compartamos loans would reduce borrowings from moneylenders. Perhaps the moneylender rates are therefore not materially different to those of Compartamos? Yunus “never imagined that one day microcredit would give rise to its own breed of loan sharks” – is Compartamos therefore a loan shark? The authors challenge the common (and convenient) misconception that microfinance is a substitute for the moneylender.

- They measure satisfaction with access to financial services (column 8) and find no significant change. This is hardly reassuring. Those who got a loan are no more impressed with the whole banking model as those who did not.

- Obtaining a loan has a significant, but negative impact on the tendency to join an informal savings group. Compartamos loans displace savings groups. Is that good or bad? It depends on the terms of the savings group I suppose.

- A mysterious line in the table which recurs in most tables is labelled “number missing”, referring to the number of clients excluded from the sample for some (usually unstated) reason. These are not trivial numbers: 9 respondents were missing from the question regarding savings group membership, but 2.484 (15%) were missing from the question about whether formal credit would be their first port of call if they needed a loan. I found no explanation of why the response rates varied so widely.

Table 4

This is one of the most interesting tables to see what the authors do and do not discover. For example, whether the client has a business or not has almost no impact on the outcome of the loan. Their claim that these loans helped businesses to grow originates in the third column: “a 0.8 percentage point increase on using loan proceeds to grow a business”. Did I read that correctly? 0.8% means only an additional 8 in every 1.000 clients used the loan to grow a business? Sure, it’s better than zero, but not a lot. The average for the sample (not explicitly mentioned, but visible in the table, column 3) is that 95% did NOT use the loan to grow a business – a disappointing result, and the fact that this got marginally better is hardly cause for celebration. Is this really one of the key findings of how beneficial microfinance is? And growing a business does not necessarily imply the business benefitted anyone, particularly if net profit declines, or if there is a negative impact upon non-borrowing vendors in the region.

Taking a loan had almost no impact on number of employees, i.e. zero employment creation. Taking a loan increased revenues, but also increased expenses by a comparable amount. The overall impact on profit was slightly negative, and not statistically significant. Hardly cause for celebration. Work harder, but make no additional profit. Or rather, work harder and any incremental profit vanishes via interest paid to Compartamos?

The final two columns in this table assess the impact of loans upon household business income and the likelihood of having suffered a financial problem in the last year. Neither are statistically significant, but the authors explicitly point out that the coefficient for the latter was positive: “an increase of 0.7 percentage points in the likelihood that the business did not experience financial problems in the past year” – again, hardly cause for celebration.

I’m not sure what conclusions one can come to other than the impact of the loans was minimal. No evidence of harm is not the typical claim made by the mainstream microfinance sector. This is a very worrying set of statistics in my opinion. I find it unusual that the final paragraph of this section suggests “in all, the results on business outcomes suggest that expanded credit access increased the size of some existing businesses”. Glass half full once again?

Those celebrating the wonders of microcredit should take note of the findings of this paper.

Table 5

The authors concede that they found no impact on business profits or total income as a result of loans, but remind the reader of the rather modest increase in the number of clients that used a loan to expand their business (an additional 8 for every 1.000 clients). The major claim in table 5 is that 20% fewer clients had to sell assets in order to repay a loan (page 16). This 20% reduction, described as “striking”, is in fact a decline from 5% of clients having to forcibly sell assets to 4%. Although technically true I am not sure the word “striking” would have been my first choice. Worded as “the rate of firesales declined by 1 case for every 100 clients” doesn’t sound quite so dramatic.

Such descriptions leave me wondering, not for the first time, if the authors are a little too anxious to extract any positive news where possible. They discover no evidence of loans used to buy assets (in fact this is a statistically insignificant but negative factor, what happened to the proverbial sewing machine or goat that microentrepreneurs supposedly buy?). Nor do they find treatment clients buy more groceries or spend more money on family events, both of which decline but are not statistically significant. One might have thought, a priori, that clients with loans might purchase the occasional asset, particularly given the rhetoric about microfinance helping the poor to grow businesses. Think again.

Increases in school and medical expenses were not statistically significant. In fact, the only other statistically significant result in table 5 is that clients with loans bought slightly fewer temptation goods, defined as cigarettes, sweets and soda. I suppose this could be considered a good thing, but in Mexico of all countries, would it not have been wise to add junk food to the list of temptation goods? Mexico scores surprisingly highly on most measures of body mass index or obesity. But it’s a minor point.

Table 6

This table is, frankly, disappointing. There is not a statistically significant result in it. The authors’ frustration is palpable. “We do not find significant effects on any of the five measures” they openly confess. No impact on income – we already saw profit actually went down. Surely this is catastrophically disappointing: hundreds of loan officers traipsing around in the blistering heat of northern Mexico for two years lending millions of dollars to armies of poor Mexicans apparently to use to good effect in the quest to eradicate poverty, and income didn’t change. Can we finally dispose of the “poverty alleviation” claim of microfinance once and for all? Instead we have to scrape around digging up marginal impacts on secondary or tertiary factors to justify the practice at all. To put this simply – what is the point? One can imagine the authors must have been rather frustrated by this point. Endless tables and calculations, 16.560 interviews, and barely a sign of any positive impact on those that receive loans. We have the income smoothening argument as a last resort – although the evidence in favour of this is minimal.

And thus we arrive at table 7, where at last something positive is extracted from the data.

Table 7

| Factor tested |

Statistically significant

|

Positive or negative

|

| Depression |

Yes

|

Positive

|

| Job stress |

No

|

Negative

|

| Locus of control |

No

|

Unclear

|

| Trust in institutions |

No

|

Negative

|

| Trust in people |

Yes

|

Positive

|

| Life and harmony index |

No

|

Positive

|

| Economic satisfaction |

No

|

Negative

|

| Good health |

No

|

Positive

|

| Child labour |

No

|

Positive

|

| Participates in financial decisions |

Yes

|

Positive

|

| # of household decision has say in |

Yes

|

Positive

|

| # of household issues with conflicts |

No

|

Negative

|

The only factors that are statistically significant are also beneficial to the clients. However, before cracking open the champagne, let’s put these in context:

- The majority of tests discover no statistically significant impact. Observe the red sections in the table above: negative impacts on job stress, trust in institutions, economic satisfaction and domestic conflicts. None of these should be taken too seriously as they are not statistically significant, but they are of the wrong, or rather unfortunate, sign.

- Trust in people apparently improves, but one wonders how accurate a measure this is, and how it squares with the decline is participation in savings groups. Also, given that for a significant number of clients (76% in fact) this is their first experience with group loans, it is hardly surprising that their trust in other people increased marginally. It’s comparable to discovering that people’s trust in parachutes increases after their first skydive. And let’s not exaggerate the impact – it grew marginally.

- The measure “participates in financial decisions” is a mysterious one. It went up, but this is hardly surprising – the clients took out loans. That’s at least one financial decision they participated in. Footnote 29 clarifies: “the dependent variable… is a binary variable equal to one if the respondent participates in at least one of the household financial decisions…”

- Much is made of the increase in the proportion of women who participated in a financial decision. The index grows from 97.5% to 98.3%. Great, it’s in the right direction. They rephrase the improvement as the number of people who have no say in financial decisions fell from 2.5% to 1.7%, which is technically true – it fell by a third. It just smells ever so slightly of trying to extract something positive out of the results. If none of the clients had ever won the national lottery before the RCT, and one client won the lottery during the trial, would that be described as an “infinite percent increase”?

Nonetheless, the conclusion to this sub-section entitled welfare is that “the results… paint a generally positive picture of the average impacts of expanded credit” (page 18). I would add “but they are generally pretty minimal and the typical client faces neither benefit nor loss, and the entire microfinance exercise appears to impact only a very small sub-set of clients, sometimes marginally positively, sometimes marginally negatively”. They wrap up this entire part of the paper on a positive note (page 18):

“Increasing access to microcredit increases borrowing” – Increasing access to cigarettes increases smoking.

“[But this increase] does not crowd-out other loans” – in fact it increases overall borrowing. First-time heroin users report similar findings. Over-indebtedness is already a serious potential problem in Mexico.

“Loans seem to be used both for investment – in particular for expanding previously existing businesses – and for risk management” – but relatively few of the clients had an existing business, the increase in asset purchases is minimal, income and expenses both increase while profit decreases. Risk management and income smoothing are often cited as benefits of microfinance, but forgive me if I am missing something here – where is the actual evidence of such benefits?

“there is evidence of positive average impacts on business size, avoiding fire sales, lack of depression, trust, and female decision making” – but all these results are generally marginal, and there are also a number of negative impacts, while the majority of tests (and who knows how many were performed but not published?) showed no impact either way.

“There is little evidence of negative average impacts” – this is probably the least biased conclusion one can arrive at. Microfinance doesn’t do much good, nor does it do much bad.

This latter point is really the crux of this case. I wonder if it would not simply have been easier to enrol the entire group in a lottery. A few decent winners funded by a large number of people who are unlikely to really notice the loss of $1. Some good and little harm, and a whole load easier than setting up a microfinance bank. Imagine an advertisement for a new (medicinal) drug: “mostly ineffective, helps a slim minority, kills very few”.

The final section of the paper…

…Adds little to the main findings, examining the variability of outcomes (outliers basically). I found only two interesting revelations.

“The results suggest that non-business owners use the loans to pay off more expensive debt, work less, and are happier for it” (page 23).

“The main takeaway is some, albeit far from overwhelming, evidence that some people fare worse when faced with expanded access to credit. Several of the sub-groups have more negative treatment effects than positive ones, with the patterns of results for those who are poorer or without prior use of formal credit access perhaps the most eye-opening” (page 27).

Yes – read that sentence again – it’s the most vulnerable people who seem to be the most likely to suffer. I thought those were the ones we were meant to be helping? And bear in mind that Compartamos doesn’t generally lend to the very poor, i.e. this sub-set is quite small for Compartamos compared to some other institutions. And then we have their overall conclusion: despite all this evidence, “our study adds to the mounting evidence that microcredit is generally beneficial on average, but not necessarily transformative in the ways often advertised by practitioners, policymakers and donors”.

This final statement is awesome. I disagree with the first part of it – where is this mounting evidence that microcredit is generally beneficial? Perhaps, debatably, if microsavings and microinsurance are included, we could possibly say there is some evidence that microfinance is generally beneficial, at a push, but microcredit? No, I cannot agree with the authors, either in general terms, or based on the findings they themselves present. “Mediocre at best” is a fairer generalisation. But they poignantly observe that the sector is hyped – that those behind the phenomenon of microcredit have falsely advertised it. This is a finding I wholeheartedly agree with.

Who are the real beneficiaries?

According to the MixMarket data for Compartamos for the years 2011 and 2012 gross loan portfolio grew from $840m to $1.1bn, as client numbers increased from 2.234.440 to 2.495.028. Stated yield on portfolio (excluding impact of forced savings and VAT) declined marginally from 73.11% to 71.38%. Net profit after taxes also declined from $167m to $156m. This equates to a net profit of $65 per client over the year based on the average number of clients. To put this in context, this equates to a little over $1m in profit per year for Compartamos and its investors simply from the sample of clients used in this study (16.560).

PAR30, the standard industry measure for portfolio quality, worsened from 3.86% to 4.44% (an increase of 15% in one year). However, the PAR90 (loans delinquent over 90 days) increased from 2.48% to 2.64% – these are the clients who are reported to the credit bureau and handed over to a debt collection agency. This is lower than the numbers suggested in the paper, but we must also consider written-off portfolio. In 2011 Compartamos wrote-off 2.91% of its portfolio, increasing to 4.19% by 2012 (an increase of 44%, equivalent to 1 in every 24 clients).

The return on equity also declined from 33.62% to 30.5%. However, as Chuck Waterfield explains in wonderful detail, this is historically low for Compartamos. The 10-year average ROE was 53%. “Compartamos investors made a 300-to-1 return on their 7 year the day of the 2007 IPO”. Waterfield proposes an ROE in excess of 25% is in the “red-zone”. Compartamos is well within this red-zone. Shareholders certainly benefit from these activities. According to Dan Rozas, “the profits of Mexican MFIs are among the highest anywhere. This is particularly highlighted by Compartamos, which has held the title of the single most profitable large commercial MFI in the world for five of the past six years. At nearly $100 million, its annual dividend payment to investors is larger than the balance sheets of most MFIs.” And let’s not forget the $2m total package to the CEO of Accion at the time of the IPO – Maria Otero, before she shuffled through that most magnificent of revolving doors straight into the White House.

In a nutshell: investors in Compartamos make very substantial profit. Finding any benefit accruing to Compartamos clients is like finding a needle in a haystack, and as this paper demonstrates, it is possibly easier to focus on the lack of harm to clients rather than search desperately for any trivial benefit they may enjoy. Once again, the rich enjoy a feast while the poor scrape around for the crumbs under the table. Welcome to Compartamos.

Conclusion

This is an important, well-written paper. Despite every effort to paint a positive picture, the results of microcredit’s impact on poverty are a little disappointing. It would be interesting to repeat the analysis in a country such as Ecuador where interest rates are capped at 30.5%. Presumably this might leave a little more profit in the hands of the poor rather than the banks and their shareholders, and lead to some more positive results.

The paper is powerful and thought-provoking, but one must read it thoroughly and not be convinced by the upbeat abstract. I didn’t expect many positive results from Compartamos, but the lack of substantial harm is good news, as more ethical institutions could actually be doing some mild good. But is +/- 2 years really enough to capture the actual impact of microcredit upon the poor, either positively or negatively? And one must acknowledge that the design of the RCT (reasonably) obliged the authors to examine a relative un-saturated region of Mexico, where the detrimental impact of over-indebtedness is perhaps less prevalent. Had the authors examined Chiapas the results may have been radically different. See the quote below from Dan Rozas’s excellent paper on a potential looming crisis in Chiapas, at the extreme other end of the country to that studied by Karlan et al.

“In Chiapas, Mexico’s poorest state of 5 million, there are some 40 MFIs operating. Multiple borrowing is rampant, with the average urban client in the state carrying 4-5 loans, while clients with as many as 7 loans are not unheard of… The average microfinance loan size is 3.2% of per-capita GNI, but in impoverished Chiapas, that’s 8.0% of the state’s per capita income. Very roughly speaking, that translates to liabilities of at least 32% of a theoretical client’s annual income owed in short-term loans… By comparison, loan sizes in Andhra Pradesh in 2010 were 11.5% of per capita GNI, while the rate of multiple borrowing in Chiapas is as bad or worse than was the case in Andhra Pradesh. Moreover, prevailing interest rates in Mexico are some 2-3 times higher than in India, which puts far greater stress on the clients’ repayment capacity for the same amount of debt. Put together, these figures imply that the bubble in Chiapas is worse than was the case in Andhra Pradesh on the eve of the crisis.”

So, I have one niggling question about this paper. Despite the evidence presented being so mediocre in terms of the impact of microcredit, why is there an on-going positive spin throughout? The two seem at odds with one another. Naturally no explanation for this is to be found in the paper, but Reuters may provide the answer. In an article by Paige Gance, Karlan (the key author) is quoted as saying:

“Investors should be quite happy and sleep better at night knowing they’re making money and making the world a better place”.

I am not sure if I, as an investor in microfinance, would be particularly happy with these results. Some investors in Compartamos certainly made a lot of money, but does this paper describe a better world? But here, perhaps, lies the clue – the Holy Grail of the microfinance community is not necessarily to have a transformative impact on the lives of the poor, but to keep the investment dollars rolling in and to protect the (increasingly frail) reputation of microcredit. An entire industry has been created around the concept, and that encompasses not simply banks, but academics, rating agencies, investment management funds, consultants etc. Industry creation was the final justification for the existence of the microfinance sector in David Roodman’s book.

The moment the investors throw in the towel the whole pack of cards collapses. Perhaps this is why there are so many positive references to the impact of microfinance when the evidence suggests otherwise? Motivation is impossible to prove, but I ask any reader of the original paper two simple questions:

- “Don’t you just get this weird feeling that the authors are desperately trying to present the case for microfinance in any way possible?”

- “Are you convinced that indebting poor people at 110% APRs is making the world a better place?”

“Win Some Lose Some? Evidence from a Randomized Microcredit Program Placement Experiement by Compartamos Banco” by Manuela Angelucci, Dean Karlan & Jonathan Zinman, May 2013

Did you like this? Share it:

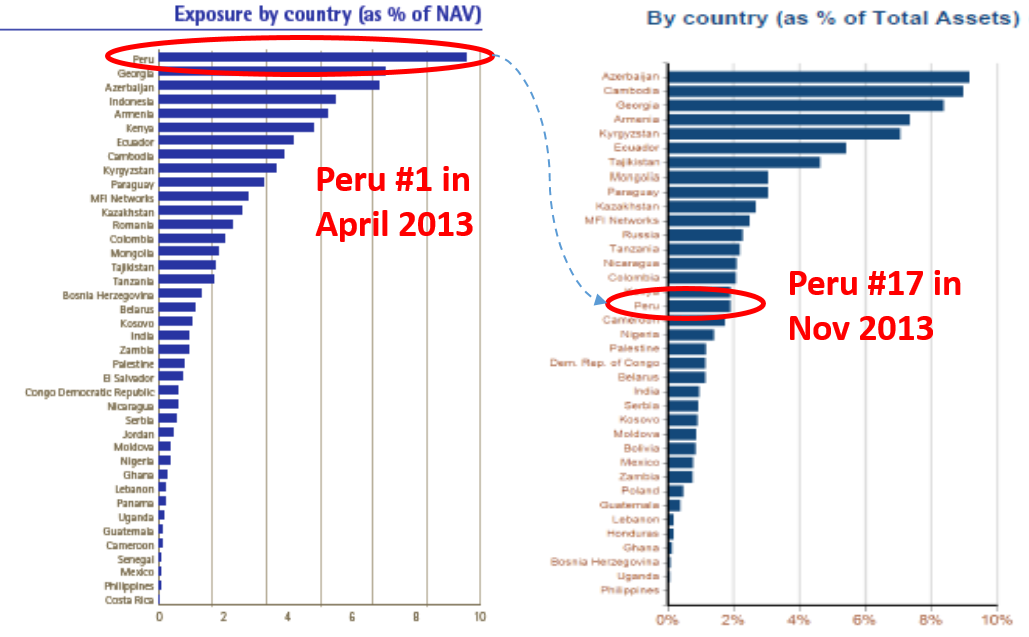

’s not exclude the broader situation in Peru. Economic growth is forecast to slow in 2014, while inflation is rising. Investors are broadly pulling out of developing countries. Civil unrest aimed against the some of the large mines has already caused riots, eerily reminiscent of the Nicaraguan “no pago” crisis. Mining revenues are declining, as is tax income. With growing over-indebtedness it is not inconceivable that more militant factions of this somewhat socialist country could trigger a similar meltdown. The images above are from a recent uprising in Peru, and the Nicaragua “no-pago” crisis. Can you spot which is which? With so many deposit-taking institutions, a run on the banks is possible were Peruvians to begin questioning the safety of their deposits.

’s not exclude the broader situation in Peru. Economic growth is forecast to slow in 2014, while inflation is rising. Investors are broadly pulling out of developing countries. Civil unrest aimed against the some of the large mines has already caused riots, eerily reminiscent of the Nicaraguan “no pago” crisis. Mining revenues are declining, as is tax income. With growing over-indebtedness it is not inconceivable that more militant factions of this somewhat socialist country could trigger a similar meltdown. The images above are from a recent uprising in Peru, and the Nicaragua “no-pago” crisis. Can you spot which is which? With so many deposit-taking institutions, a run on the banks is possible were Peruvians to begin questioning the safety of their deposits.

Did you like this? Share it:

Did you like this? Share it: